Once-in-a-generation financial crisis is coming (From Porter & Company)

Key Points

- ServiceNow is on track for a stock split that investors should heed: stocks that split tend to see their share prices trend higher.

- AI demand drives results that, in turn, drive steadily increasing shareholder value.

- Analysts and institutional trends indicate solid market support and a potential 20% upside.

ServiceNow’s (NYSE: NOW) 5-for-1 stock split is a signal for investors to buy, as the reasons behind the decision point to a sustained uptrend in the stock price.

Already up more than 100% over the past three years and quadruple digits over the long term, this stock can continue to climb higher because its entrenched technology business is in demand, growing, and driving shareholder value.

Ultimately, the split is intended to make the shares more accessible, as a $1,000 price tag is hard for most investors to swallow. Not that the business isn’t worth the money, only that $1,000 stocks make portfolio diversification and regular purchases difficult at best.

The Republican party is falling apart (Ad)

Something unusual is unfolding inside the Republican Party — from Marjorie Taylor Greene breaking ranks to Ted Cruz calling the White House a “mafia,” and even Trump’s approval rating slipping. But veteran analyst Porter Stansberry says this isn’t really about politics at all. It’s part of a much larger shift he calls The Final Displacement — a historic economic and social realignment already impacting millions of Americans. His new documentary explains what’s driving it and how to prepare before it accelerates further.

Watch The Final Displacement to see what’s really happening behind the scenes

ServiceNow: Beat-and-Raise Quarter Affirms Outlook for 20% Upside

ServiceNow had a solid quarter in Q3 with AI demand driving its business. The company reported strength across its product groups, with net revenue of $3.41 billion, up nearly 22% year-over-year. The strength was slightly better than expected, driven by an 18% increase in large clients, resulting in significant bottom-line outperformance. Internal indicators, including remaining performance obligation (RPO) and current RPO, are up 24% and 20.5%, respectively, suggesting strength will continue in upcoming quarters and growth may accelerate.

Margin news is also favorable. The company experienced margin pressure at the gross level, but offset it through spending controls and efficiency. The net result is a 180 basis points improvement in the operating margin and adjusted EPS of $4.82, $0.55 better than MarketBeat’s reported consensus estimate. That is nearly 1300 basis points better than forecast and is compounded by guidance that expects the strength to continue. The company forecasts revenue to run at a solid 20% pace for the year, up from the prior guide and ahead of the consensus.

The response from analysts was mixed, including one price target increase and one decrease within the first 18 hours of the release, but it reveals an optimistic group. The trends include increasing coverage, a solid support base with more than 33 analysts tracked by MarketBeat, a firm Moderate Buy rating, and an uptrend in the price target. It forecasts a 20% upside relative to the critical support target, as of late October, and the fresh revisions align with it.

ServiceNow Drives Share Price Increases With Equity Gains

ServiceNow neither pays dividends nor repurchases significant amounts of shares, choosing instead to invest in its business. The critical takeaway is that its investments have been paying off for years, driving steadily increasing equity that lifts the stock price over time.

The balance sheet highlights at the end of Q3 reflect the intensity of 2025 investment, with cash equivalents and total assets down year-to-date, but this is offset by reduced liabilities, steady debt levels, and a nearly 18% increase in equity. In 2026, continued reinvestment and high demand for AI automation and business services are expected to lead to substantial equity gains.

Institutional activity reveals that ServiceNow’s business strategy aligns with its interests. The data shows a nearly 88% ownership rate, and the group has been buying on balance all year. There was some caution ahead of the Q3 release, as reflected in October activity, which was light but still selling. The group will likely revert to a more bullish tone now that the results and guidance are in.

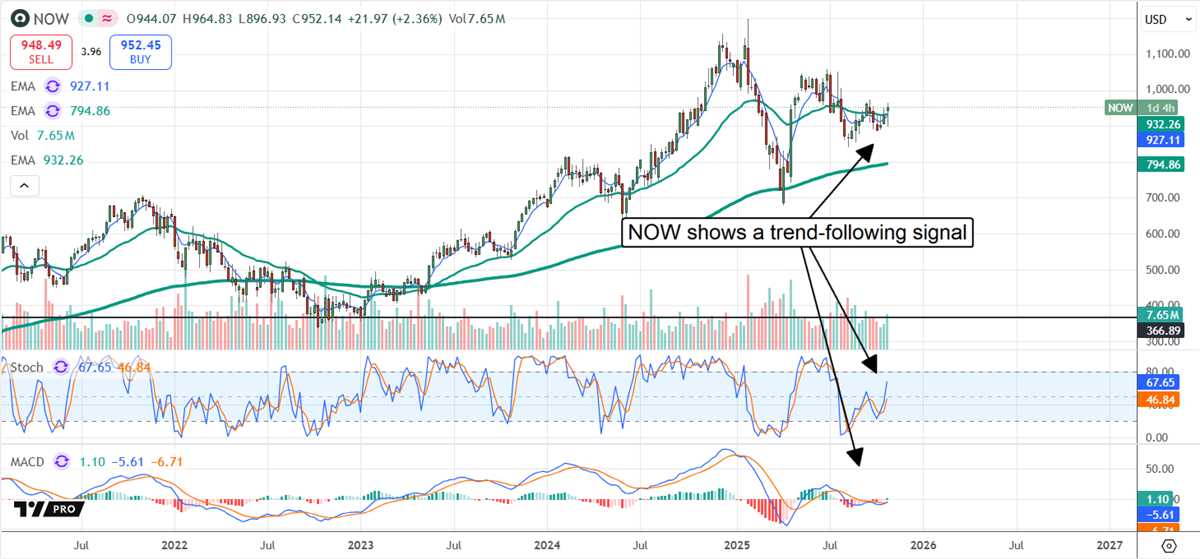

The chart shows a positive outlook. ServiceNow’s stock has mostly consolidated over the past year but remains in an overall uptrend. October trading shows strong support at critical moving averages, and the indicators have swung into a trend-following signal. The likely outcome is that NOW stock will advance in November, potentially reaching the $1,050 to $1,100 range before the early December stock split.

Read More:

- Is Lemonade Stock Set for a Big Squeeze After Earnings?

- Trump's Law S.1582: $21T Dollar Revolution Coming (From Brownstone Research)

- Caterpillar Stock Could Top $650 by Year’s End

- This gold stock is STILL undervalued by 80%... (From Golden Portfolio)

- Is Beyond Meat a Buy After Meme Stock Surge? Analysts Say No

- ABBV Stock: $250 May Be the New Floor After Big Q3 Earnings Beat

- Super Micro's Moment of Truth: A Growth Story Under Pressure